REVIEW: Boom, by Byrne Hobart and Tobias Huber

Boom: Bubbles and the End of Stagnation, Byrne Hobart and Tobias Huber (Stripe Press, 2024).

I’ve called fifteen of the last two bubbles correctly.

There’s something incredibly satisfying about standing aloof, impartial, and above it all while everyone else is losing their heads about the latest craze. You sit there, refreshing Zerohedge, sipping your chablis, shaking your head and tut-tuting or tsk-tsking at all the poor deluded saps getting rich around you. “What pathetic, brainwashed idiots,” you smirk as the stock market reaches yet another all-time high, “don’t they know that the crash is coming any day now?” Sometimes the crash does actually come and your put options become worth something. We won’t look too carefully at how my returns compare over the long haul to those of the S&P.

Even when I’m not being a permabear, I tend to invest in boring and diversified ways. But wait a minute! There’s another sector of economic life where my instincts and intuitions run in exactly the opposite direction. Because if you took modern portfolio theory and applied it to your career, clearly the only “rational” choice is to go into a field that lets you hedge and diversify your career across many different companies and sectors. In other words, you should go into consulting or finance or law. In fact, that’s precisely what an ever-growing proportion of elite college grads are doing, which I complained about at length in a review of a different book from Stripe Press.

If you don’t buy this analogy yet, consider a well-informed participant in a stock market bubble, shitcoin frenzy, or similar. Why would somebody who’s in it for more than the vibes pay a huge amount for an asset that seems, objectively, to be worth much less? On some level, they must believe they see something others don’t. But that means they’ve formed specific, falsifiable theories about the future and learned things about the world that made them decide “this time is different.” Whether they’re right or wrong, this is the exact opposite of the generalist, domain-neutral approach to talent allocation that I revile.

It’s very similar to the decision to start or join a startup, or to work for a business that does something tangible in the world. These, too, are bets that a specific set of futures will come to be — and betting years of your life on a company is much riskier than betting a few thousand dollars on Gamestop! Conversely, going into a generalist field where you organize and allocate the labor of others is like buying index funds: a way to float along with the current without expressing an opinion about how things will turn out.1

Now that I’ve strengthened the analogy, maybe I’ve made the other side sound too good! Index funds earn great returns, and people in finance, law, and consulting tend to do all right — so what exactly is the problem? Yes, taking the portfolio theory approach to any kind of investment, whether in the markets or in your career, can turn out very well for an individual. The trouble comes when everybody starts to do it: your society stagnates.

I won’t attempt to recap here the many arguments that have been made recently about whether and how our society is stagnating. You could read this book or this book or this book. Or you could look at how economic productivity has stalled since 1971. Or you could puzzle over what else happened in 1971. Or you could read Patrick Collison’s list of how fast things used to happen, or ponder how practically every new movie these days is a sequel, or stare in shock at declines in scientific productivity. This new book by Byrne Hobart and Tobias Huber starts with a survey of the most damning indicators of stagnation, moves on to suggest some underlying causes, and then suggests an unexpected way out.

Their explanation for our doldrums is simple: we’re more risk averse, and we don’t care as much about the future. Risk aversion means stagnation, because any attempt to make things better involves risk: it could also make things worse, or it could fail and turn out to be a waste of time and money. Trying to invent a crazy new technology is risky, going into consulting or finance is safe. Investing in unproven startups or speculative bets is risky, investing in index funds is safe. Trying to overturn the scientific consensus is risky, keeping your head down and publishing papers that don’t say anything is safe. Producing challenging new art is risky, spewing an endless stream of Marvel superhero capeshit is safe. Even if, in every case, the safe option is the “rational” choice for an individual actor in maximin expected value terms, the sum total of these individually rational choices is a catastrophe for society.

So far this is a lame, almost tautological, explanation. Even if it’s all true, we still haven’t explained why people are so much more fearful of failure than they used to be. In fact, we would naively assume the opposite — society is much richer now, social safety nets much more robust, and in the industrialized world even the very poor needn’t fear starvation. In a very real sense, it’s never been safer to take risks. Failing as a startup founder or academic means you experience slightly lower lifetime earnings,2 while, in the great speculative excursions of the past, failure (and sometimes even success) meant death, scurvy, amputations, destitution, children sold into slavery or raised in poorhouses — basically unbounded personal catastrophe. And yet we do it less and less. Why?

Well, for starters, we aren’t the same people. Biologically, that is. We’re old, and old people tend to be more risk-averse in every way. Old people have more to lose. Old people also have less testosterone in their bloodstream. The population structure of our society has shifted drastically older because we aren’t having any children. This not only increases the relative number (and hence relative power) of older people, it also has direct effects on risk-aversion and future-orientation. People with fewer children have all their eggs in fewer baskets. They counsel those kids to go into safe professions and train them from birth to be organization kids. People with no children at all are disconnected from the far future, reinforcing the natural tendency of the elderly to favor consumption in the here and now over investment in a future they may never get to enjoy.

Old age isn’t the only thing that reduces testosterone levels. So does just living in the 21st century. The declines are broad-based, severe, and mysterious. Very plausibly they are downstream of microplastics and other endocrine-disrupting chemicals. The same chemicals may have feminizing effects beyond declines in serum testosterone. They could also be affecting the birth rate, one of many ways that these explanations all swirl around and flow into one another. Or maybe we don’t even need to invoke old age and microplastics to explain the decline in average testosterone of decisionmakers in our society. Many more of those decisionmakers are women, and women are vastly more risk-averse on average.3

Yikes, this book review is getting too edgy! Let’s retreat to the safer ground of monetary policy. One of the best sections of Boom is a whip-smart and tightly-argued few pages connecting hyper-financialization and central bank interventions to our twin themes of risk aversion and present focus.4 It’s all very convincing, but also rather depressing, because what can you (yes, you) do about microplastics in the bloodstream or the abandonment of the Bretton Woods financial system or the fact that none of your peers are reproducing, or any of the other determinants of our apparently rather overdetermined stagnation? The answer is “virtually nothing.” So is this a counsel of despair? Should you stick your head in the sand? Or become a consultant and try to enjoy your time in our stagnating, declining society?

No. You can’t fix any of that stuff, but you can participate in a nice bubble instead.

Aren’t bubbles bad? Well yes, and you probably thought of some of the ways they’re bad at the start of this review, when I was lauding them for representing concrete, falsifiable, specific theories about the future. Bubbles involve lots of people acting irrational and crazy, driven by FOMO (fear of missing out) to pour their savings into highly speculative endeavors with some tiny chance at a payoff in the future. That does sound bad. On the other hand, if your society was dying from risk-aversion and present focus, doesn’t it also sound like a speculative frenzy might act as a weird sort of medicine?

If a bubble is defined as a group of people whipping each other up into a FOMO-driven frenzy and bidding an asset up to a price that’s unjustifiable on economic fundamentals, how can that ever be a good thing? Well, we’re assuming that eventually the price comes crashing back down and some sucker is left holding the bag. In other words, we’re assuming that it’s a failed bubble.5 But what if the price is initially unjustifiable, but somehow the bubble is a self-fulfilling prophecy and at a certain point the price becomes a good one, or even too low?

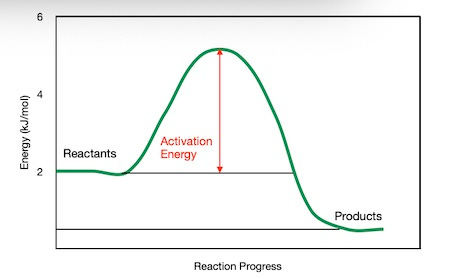

An easy example of this is any business with network effects, where the value of the product is proportional to the number of other people using it — like a social network or a new currency. It might be objectively stupid for the first person, or the first thousand people, or even the first million people, to start using it. But under bubble conditions they might not be thinking straight, and a ton of people might adopt the product even though it doesn’t make any sense to do so. Paradoxically, this causes it to make sense and suddenly the formerly-ridiculous price is justified after all. The more general case of this phenomenon is called activation energy: sometimes a physical system, whether it’s a chemical reaction or a new social phenomenon, just needs a little kick to get going. Bubbles are very good at providing those kicks.

Another important sort of activation energy in economic development is parallel progress. Sometimes, there’s a whole collection of businesses that don’t make any sense unless the other ones already exist. For example, it doesn’t make sense to start the first car company unless there are gas stations, but it doesn’t make sense to build gas stations unless lots of people have cars. A mutual dependency like this might never get off the ground unless both sides decide to YOLO it and assume that somebody will build the other half by the time they get there. A bubble might help make that happen. A related phenomenon is clustering. In a past review I talked at length about why so many industries end up geographically concentrated. A bubble causes temporal concentration — clustering in time, rather than space, but with many of the same benefits!

The bulk of this book is Hobart and Huber opening our eyes to just how many of the greatest triumphs of the 20th century actually exhibited bubble-like dynamics if you take a closer look. We all remember the failed bubbles — the Tulipomania, the late 80s AI craze, the 2008 housing crisis, and so on — but we tend not to remember the successful bubbles as bubbles, and we retcon away how giddy and irrational their early stages actually were.

For starters, every successful new business was once a kind of bubble. All of the dynamics are there: for instance, the stock options are worthless at the start, but by attracting talent become a self-fulfilling prophecy. Walk into a growing startup and the “reality distortion field” is palpable. Everybody sees a possible future, and a path to bringing that future into the present, and shakes their heads at the poor clueless fools who don’t see how, soon, everything will change. Startups have cult-like dynamics in multiple ways. There’s a cottage industry in making fun of startup people who want to change the world with B2B SAAS, but this misses the point — it only works because they believe that. You only found or join a startup because you really, truly believe that your stupid app will change the world, and sometimes that belief makes it so. And finally, crucially, there is no “accountability.” Accountability is a form of reality check, and reality checks are very bad for bubbles. Startup leadership tends to be dictatorial. In theory “the market” could provide some accountability, but market discipline is tenuous when it comes to startups, because the company gets cash infusions from investors and because it can pick and choose strategic moments for a “mark to market” of its valuation.

Okay, so social phenomena that have nothing to do with the stock market can look very analogous to bubbles. But Hobart and Huber’s list is a bold one: the Manhattan Project, the Apollo Program, the growth of semiconductor manufacturing, the golden age of corporate R&D, the fracking revolution,6 and Bitcoin. With the exception of the last item, you might be shocked to hear that each of those episodes involved extreme bubble dynamics: FOMO, messianism, parallel progress, time compression,7 and so on. They also all involved one or more charismatic leaders with cult-like followings and zero accountability to any sort of external authority.8 Yes, they were all bubbles.

In fact, once you start thinking about the world this way, you start seeing bubbles everywhere. The heretical philosopher of science Paul Feyerabend once made waves by arguing that new scientific theories often contradict the best available evidence (my review of Einstein’s Unification is a detailed investigation of a notable instance of this). There could be lots of reasons why: maybe the new theory hasn’t yet accumulated epicycles that explain away anomalous data like the older theory has, or maybe some of the experimental data that supports the dominant paradigm is fraudulent or innocently wrong. But the point is that, in Feyerabend’s view, the new theory — even if it is a better theory — initially appears to be a much worse theory. So it needs to defend itself. This basically happens via its supporters and adherents ignoring conflicting data, firing each other up in a cult-like atmosphere, and generally acting like a bunch of NFT-obsessed baboons. New scientific theories are bubbles.

But maybe the best bubbles are on a more intimate scale. Evolutionary psychologists tell us that love is a way to fool another by first fooling yourself.9 I’m too much of a romantic to believe this theory, but having read this book I do now think love is a kind of bubble. If you think about it, pair-bonding is miraculous. You somehow go from not even knowing somebody to having the rest of your life irrevocably intertwined with theirs. How does this happen? You fall in love. You become temporarily convinced that that person is the greatest human being ever, you can’t stop thinking about them, you experience FOMO, time compression, the works. And if you’re lucky, this all provides the activation energy you need to build a life together, to become the best people in the world for each other, to start living up to each others’ overhyped expectations. Falling in love is a bubble.

And this sort of bubble also gives us an interpretive key for all the others — and to understanding the broader crisis of our civilization. Because marriage is, at its root, about sacrificing optionality, incurring opportunity cost, and committing to something with the knowledge that you could be giving up something better in the future. In this, it’s a synecdoche for the whole host of economic choices that Hobart and Huber want us to make. There’s something eerily similar between the people who are permanently on the dating market and the people who are permanently in grad school. Perhaps what we’re dying from isn’t society wide risk-aversion, but society-wide commitment phobia. The good news is that bubbles can help with that too.

I guess in this analogy, endlessly attending more and more graduate programs and post-grad programs and fellowships and internships is like sitting in cash? The ultimate in commitment anxiety.

And given the logarithmic hedonic utility of additional money and fame, that hurts even less than it sounds like it would.

I’m on the record as a moderate skeptic of the Federal Reserve, but I don’t really know what I’m talking about, whereas Hobart has been thinking and writing about financial markets for decades.

Actually, even failed bubbles can leave some very useful economic wreckage lying around, and might still be a net positive for society. Hobart and Huber give a number of examples, but the one that always springs to mind for me is the fiber optic buildout of the late 90s.

There were a number of moments when reading this book almost made me shout with joy, but one of them was certainly the footnote in the fracking section that discusses Xenophon. It’s that kind of book.

At one point, Hobart and Huber relate “bubble time” to kairos and chronos, and to the cyclic vs. linear conceptions of time. As I said, it’s that kind of book.

One of my favorite books on space policy is W.D. Kay’s classic Can Democracies Fly in Space?, the Straussian reading of which is that the answer is “No” and that golden age NASA proves it because it was an absolute dictatorship under Administrator James Webb, who skillfully shielded the organization from any sort of democratic accountability. Bullish for SpaceX.

The argument, which I have heard from actual professors of evolutionary psychology, goes something like this: (A) obviously it’s in everybody’s interest to trade up to a higher-quality mate as soon as possible, but (B) since everybody knows that everybody else is thinking that, we’re programmed to be ultra-skeptical of lovers making promises, therefore (C) when trying to woo somebody you need to be as convincing as possible that you’re in it for the long haul and only care for them, and finally (D) the best way to sell somebody on a lie is to believe it yourself, so we “fall in love” as a way of tricking ourselves into believing we’re committed, so we can then trick others.

This has the character of a lot of evolutionary psychology arguments — superficially plausible, but no actual evidence for it, and kinda falls apart if you think about it too hard.

This is what I love about this Substack: That I get to read about "that" kind of book. Boom's thesis is so refreshingly heterodox and it's probably true. I have to think about Isaacson's biography of Elon Musk, in which he displays example after example of Elon and his teams going absolutely all-out on a seemingly impossible quest - and more often than not succeeding in the end, after a world of pain and sometimes endless delays. This is the aggressive energy that ultimately changes the world and will shape our future. I'm not cut out for it, but I have immense respect for those who are.

The argument that more well-off and comfortable people should take more risks seems backwards, unless the risks aren't all that bad and they're bored or something? I think you're missing some important components of risk-taking: (1) What are the alternatives? In societies before modern medicine, safety practices, and insurance, there were more immediate dangers everywhere, probably resulting in a more casual acceptance of risks. Nowadays, with fewer risks to worry about day-to-day, we get excited about rather subtle, long-term risks. (2) Sometimes they have romantic notions of what it would be like. This probably explains why boys would run away to become soldiers or sailors, which doesn't happen so much anymore.

We could also study the people who *do* take more risks nowadays, and what motivates them. Immigrants come to mind. Wars and economic devastation are motivating, but there are also strivers.

The connection to having a family seems a little odd, too. Aren't risk-takers stereotypically young, single men? It was certainly true in California in 1849.